- Accounting and

- Business

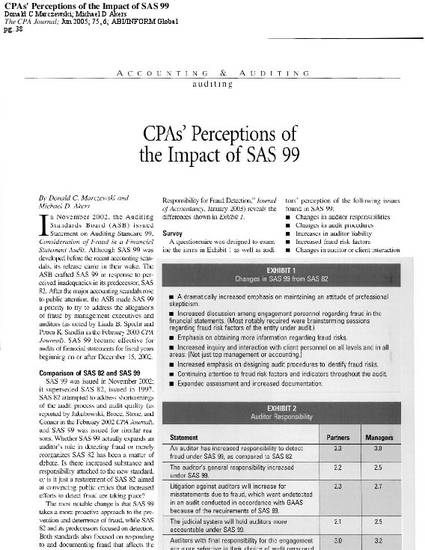

In November 2002, the Auditing Standards Board (ASB) issued Statement on Auditing Standard 99, Consideration of Fraud in a Financial Statement Audit. Although SAS 99 was developed before the recent accounting scandals, its release came in their wake. The ASB crafted SAS 99 in response to perceived inadequacies in its predecessor, SAS 82. A questionnaire was sent to a random sample of 300 Wisconsin CPAs selected from the membership of the Wisconsin Institute of CPAs, which included 150 partners and 150 managers from Wisconsin public accounting firms. The response rate was 35%, with an almost equal balance of partners and managers. Respondents were asked to rate each of the 29 statements in the questionnaire on a scale from 1 to 5, with 1 representing that the respondent strongly agreed with the statement, while 5 represented that the respondent strongly disagreed. If any significant differences existed between the responses provided by the partners and by the managers, a statistical t-test was conducted for each question. The results were grouped and presented in the following five categories: 1. auditor responsibility, 2. client interaction and public opinion, 3. fraud risk factors and audit effectiveness, 4. workpaper documentation, and 5. audit procedures. Results of the poll are presented.

Available at: http://works.bepress.com/michael_akers/32/

Published version. The CPA Journal, Vol. 75, No. 6 (June 2005): 38-40. Permalink. Reprinted from The CPA Journal, June 2005, © 2005, with permission from the New York State Society of Certified Public Accountants.