- Social sciences,

- Credit rating change,

- Financial markets,

- Information dissemination,

- Information propagation,

- Stock market liquidity

This dissertation consists of three essays which examine information flows through financial markets and across firms, and investigates the factors affecting the process of information dissemination. The first essay examines whether the announcement of a credit rating change for a given firm contains information pertinent to the valuations of intra-industry peer firms. I identify an information spillover effect on peer firms surrounding credit rating downgrades. Further, I find that the post-announcement spillover effects are indicative of an overreaction in the market’s response to the downgrade announcement. Peer firms exhibit predictability in their post-announcement returns as a function of their relative transparency.

The second essay explores the relation between instances of credit rating initiations and stock market liquidity. Traditional finance literature holds the view that liquidity is impaired as a function of information asymmetry. Additionally, that credit ratings have been shown to reduce information asymmetry. This study uses instances of new credit ratings to examine the change in stock market liquidity surrounding the announcement of the new rating. My results suggest that rating initiations improve in the liquidity of the newly rated firm’s equity and that managers exploit this price support through seasoned equity offerings.

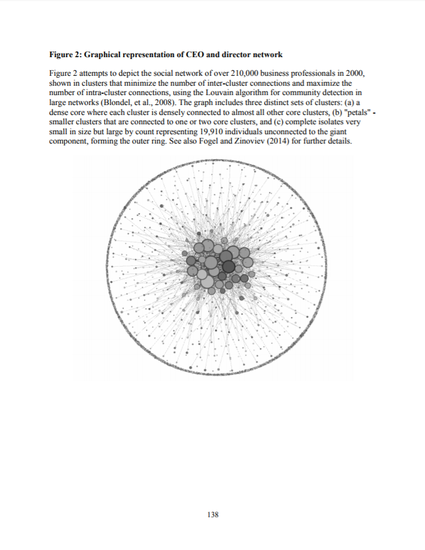

The third essay investigates information flows through the Social networks of board members. I find that the degree to which a CEO and her directors overlap in Social communities affects the governance of the firm and that these effects are conditional upon the adverse reputation costs faced by the board. For firms whose boards face relatively lower (higher) potential adverse reputation costs to bad behavior, clustering is associated with poorer (better) governance and greater (lesser) expropriation by managers.

Available at: http://works.bepress.com/garrett_mcbrayer/4/