Presentation

Exploring the PCAOB’s Standard-Setting Process

Spark AAA 2020 Meeting

(2020)

Abstract

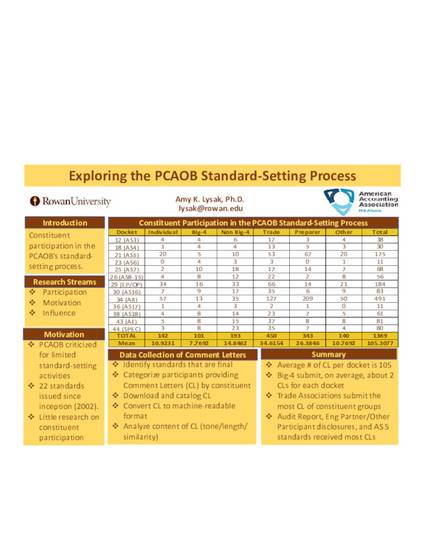

This research explores the standard-setting process of the PCAOB. The PCAOB has faced much criticism in its formative years as it standard-setting activities were limited with its focus on inspection. It has issued just over twenty auditing standards since its inception. As part of its due process, the PCAOB solicits feedback from the public on its proposed auditing standards. Constituents are then able to provide feedback (in the form of a comment letter) on the proposed standard; which the PCAOB may or may not consider as it finalizes a standard. There has been little research that identifies and evaluates the participation of its key constituents for the PCAOB’s standard-setting process. This research compiles the comment letters submitted and made public by the PCAOB on their website to evaluate participation by standard and constituents. Preliminary results show that trade associations and preparers of financial statements provide the largest amount of comment letters for the sample analyzed. In addition, on average, 105 comment letters are submitted for each rule-making docket. Future research will evaluate the motivations for constituents’ participation as well as whether constituents have influenced the PCAOB’s standard-setting process.

Disciplines

Publication Date

April 26, 2020

Comments

https://creativecommons.org/licenses/by-nc/4.0/

Citation Information

Amy Lysak. "Exploring the PCAOB’s Standard-Setting Process" Spark AAA 2020 Meeting (2020) Available at: http://works.bepress.com/amy-lysak/4/

Creative Commons License

This work is licensed under a Creative Commons CC_BY International License.